This is part of a series on Anti-money Laundering (AML) and Combating the Financing of Terrorism (CFT) in Suriname, South America.

Let us dive in to understand the intricacies.

Under the leadership of President Chandrikapersad Santokhi, Suriname,, a South American nation, has been strengthening its anti-money laundering (AML) efforts. Since 2020, the administration has prioritised tightening enforcement measures and regulations to reduce dependence on a cash-based economy and build a more transparent and resilient financial system.

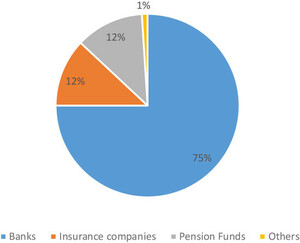

Suriname’s financial sector is crucial in combating money laundering and terrorism financing. Banking institutions dominate the sector, accounting for 75% of total assets. This concentration necessitates robust sectoral responses to mitigate financial crime risks.

President Chandrikapersad Santokhi and Governor Maurice Roemer of the Central Bank of Suriname

Suriname’s financial landscape comprises ten primary banks, insurance companies, pension funds, credit unions, and money transfer offices. The banking sector is the most significant, with a total asset balance of around SRD 22 billion as of 2018. The country’s economy heavily relies on natural resource exploitation.

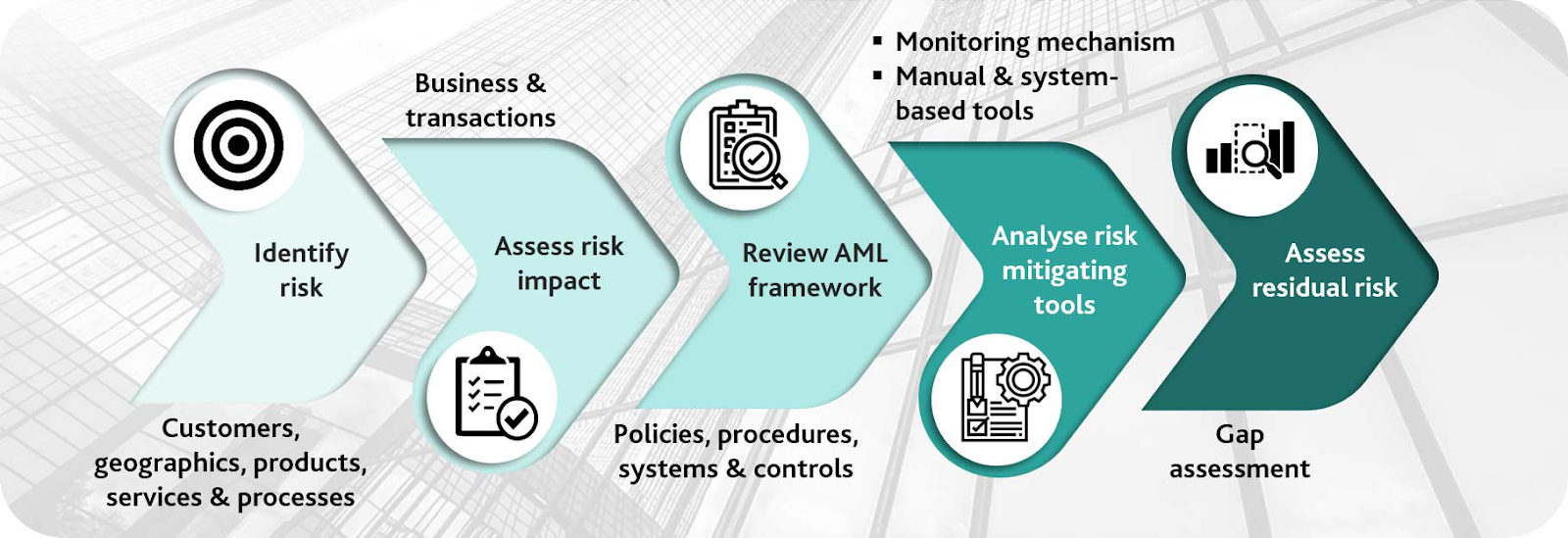

Suriname has established a regulatory framework for AML/CFT, overseen by the Central Bank van Suriname (CBvS). This framework requires financial institutions to adhere to international standards through laws and guidelines.

Financial institutions must conduct risk assessments to identify operational vulnerabilities, particularly in sectors like natural resources. They also implement compliance programs and staff training on AML/CFT obligations to enhance awareness and enable effective detection and reporting of suspicious activities.

The focus is on fostering collaboration among financial institutions, regulatory bodies, and law enforcement agencies to enhance the detection and prevention of financial crimes.

Table of Contents

Financial Institutions

Financial institutions (FIs), such as banks, insurance companies, brokerages, investment firms, and credit unions, accept deposits, provide loans, and offer financial services. Government authorities heavily regulate them due to their central role in the economy, responsibility for consumer funds, and financial system stability.

In Suriname, commercial banks, offshore banks, the Central Bank, and microfinance institutions are essential financial institutions. Commercial banks, including foreign and government-owned ones, are subject to AML/CFT regulations. Offshore banks cater to non-residents and can be a focal point for AML/CFT due to cross-border activities.

Role of Financial Institutions

Financial institutions (FIs) are crucial for economic growth. They facilitate financial transactions like savings mobilisation, credit provision, and payment processing. They also manage risk through insurance and derivatives. FIs are subject to strict regulatory frameworks like anti-money laundering and counter-terrorism financing to ensure compliance and protect against financial crimes.

Image source: AML framework

Suriname’s financial institutions (FIs) are crucial for the economy, providing essential services like banking, insurance, and investment management. De Surinaamsche Bank (DSB), one of the oldest and largest banks, offers a range of financial products. Regulated by the Central Bank of Suriname, FIs comply with national and international financial standards, ensuring stability and effectiveness for the country’s economic health and development.

Image source: Distribution of Financial Sector Assets

Case Example for FIs in Suriname

Due to economic instability and institutional corruption, Suriname’s financial institutions face challenges in adhering to anti-money laundering and counter-terrorism financing regulations. This provides insight into operational realities and regulatory obstacles in the evolving financial system. An understanding of the context is essential here.

Composition of the Financial Sector: As of December 2019, Suriname’s financial sector included ten commercial banks, 13 insurance companies, 19 credit unions, 33 pension funds, and various money exchange services. The banking sector remains the most regulated segment, reflecting lessons learned from previous AML operations during Desi Bouterse‘s politically turbulent times.

AML Compliance Challenges: Suriname’s National Risk Assessment (NRA, 2021) reveals inconsistent enforcement of Anti-Money Laundering (AML) legislation, with significant gaps in understanding and implementation among authorities, including the Foreign Exchange Commission, causing FIs to struggle effectively.

Image source: Financial institutions

Historical Context of Corruption: Corruption in Suriname, particularly during the tenure of former President Dési Bouterse, has significantly impacted financial institutions, leading to legal and operational issues. The Santokhi administration focuses on anti-corruption efforts to revive weakened law enforcement institutions, including implementing a 2017 anti-corruption law and forming an anti-corruption commission. They are also seeking international assistance to combat drug trafficking and improve national security.

High-Risk Sectors Identified: Suriname’s NRA has identified high-risk sectors for money laundering, including illegal gold, timber, used cars, and small-scale jewellery businesses, urging financial institutions to intensify scrutiny.

Future Prospects and Recommendations: Suriname’s potential oil reserves present opportunities and challenges for its financial institutions. Effective governance, transparency, and rigorous AML measures are crucial for external financial support and growth, emphasising the need for proactive governance.

Suriname’s financial institutions face regulatory challenges and historical corruption, but also potential for reform, crucial for maintaining the country’s financial system’s integrity and stability.

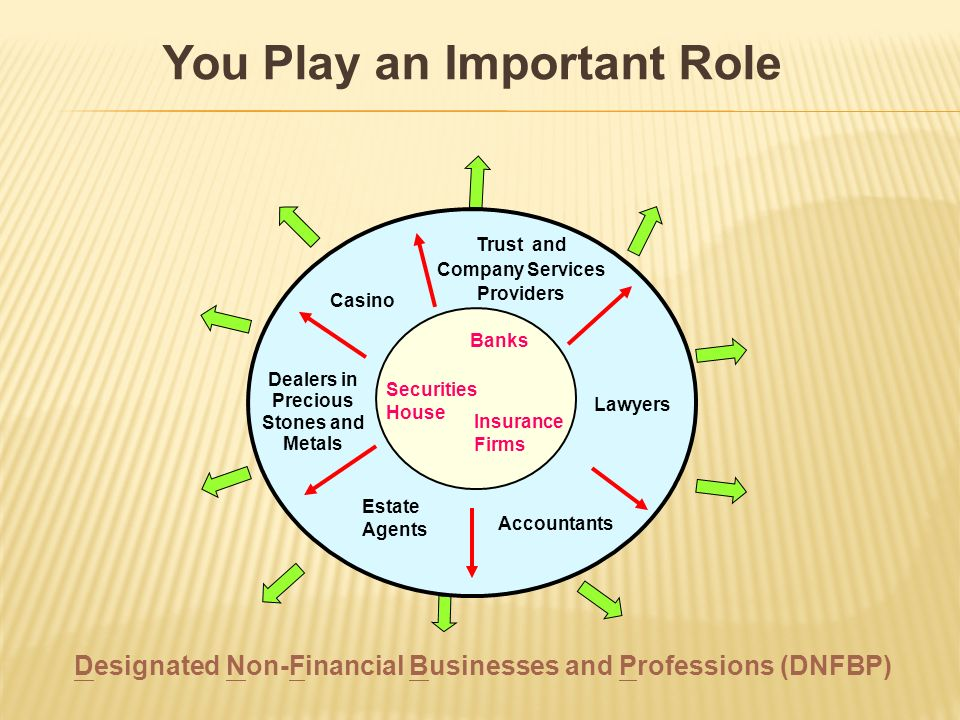

Designated Non-Financial Businesses and Professions (DNFBP)

DNFBPs, including real estate agents, accountants, lawyers, casinos, and precious metal dealers, are a group of non-financial entities that can be exploited for money laundering or terrorist financing. Despite not being financial institutions, DNFBPs play a crucial role in identifying and reporting suspicious activities due to their transaction nature.

Image source: Stakeholders in DNFBPs

Importance of DNFBPs

DNFBPs, often managing high-value transactions, are vulnerable to illicit financial activities due to their role as gatekeepers in the AML/CFT framework. They identify potentially illegal transactions before they enter the financial landscape, and their compliance with regulatory obligations ensures the global financial system’s integrity.

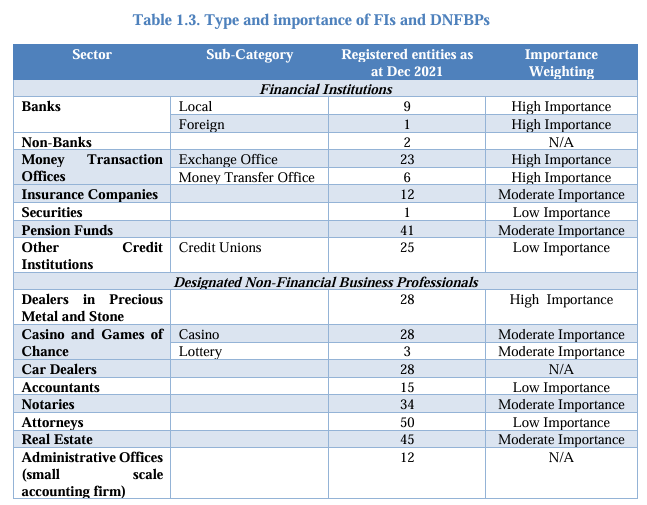

Image source: Type and importance of FIs and DFNBPs

Case Example for DFNBPs in Suriname

Suriname’s Designated Non-Financial Businesses and Professions (DNFBPs) are vital in combating money laundering and terrorist financing, particularly in sectors like real estate, casinos, and financial transaction intermediaries due to their high-risk exposure.

DNFBPs in Suriname are businesses and professions involved in high-risk financial transactions, such as real estate agents, casinos, jewellers, and lawyers and accountants, which must comply with anti-money laundering regulations and guidelines set by authorities.

Image source: Avenues for AML/CFT

In Suriname, DNFBPs must report suspicious transactions to the Financial Intelligence Unit (FIU) through Unusual Transaction Reports (UTRs). This aims to detect potential money laundering or terrorist financing activities and investigate them accordingly.

Casinos in Suriname are a prime example of DNFBPs, as they are susceptible to money laundering due to large cash transactions and anonymous betting. Regulations mandate robust customer due diligence processes, monitoring transactions, and reporting suspicious activities. For instance, if a patron demonstrates unusually high-stakes gambling, the casino must report it to the FIU for further investigation.

DNFBPs failing to comply with AML guidelines can face severe penalties, including fines and license revocation, which risks their operations and jeopardises Suriname’s financial system’s integrity, emphasising the importance of strict AML regulations.

Suriname’s FIU is enhancing compliance with DNFBPs through training programs and outreach initiatives. It aims to improve its capacity to identify and report suspicious activities, contributing to a stronger AML framework in the country.

Image source: Illegal transactions

Interaction Between FIs and DNFBPs

Financial institutions and the Department of Financial Institutions frequently collaborate within financial ecosystems. DNFBPs provide services to ensure compliance with regulations governing FIs, such as AML and CFT regulations, thereby ensuring comprehensive financial security and preventing illicit fund infiltration into the economy.

Financial Institutions (FIs) and Designated Non-Financial Businesses and Professions (DNFBPs)

Financial Institutions (FIs) and Designated Non-Financial Businesses and Professions (DNFBPs) are crucial in combating money laundering and terrorist financing globally. They must implement robust AML/CFT measures, such as customer due diligence, transaction monitoring, and reporting of suspicious activities. FIs include banks, insurance companies, and securities firms, while DNFBPs include real estate, legal services, and casinos.

Importance of Financial Institutions and DNFBPs

Suriname’s Anti-Money Laundering and Counter-Terrorist Financing framework comprises financial institutions, designated non-financial businesses, and professionals responsible for implementing measures like customer due diligence, transaction monitoring, and reporting suspicious activities.

Image source: AML Checks

Inconsistencies in Understanding Obligations

The Caribbean Financial Action Task Force’s (CFATF) Mutual Evaluation Report reveals significant inconsistencies in understanding and meeting AML/CFT obligations among entities, potentially compromising the framework’s effectiveness in preventing money laundering and terrorist financing.

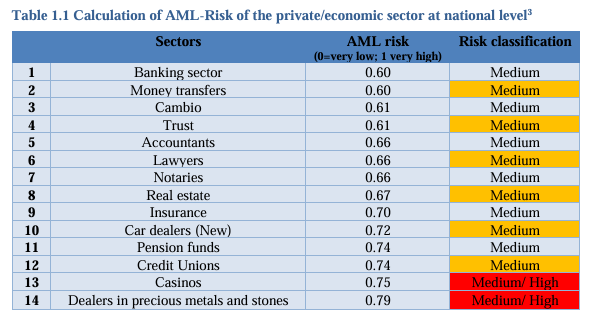

Image source: Sectors in Suriname – AML risk classification

The image displays a table assessing anti-money laundering (AML) risk across different financial sectors, including banking, money transfers, and trusts. It provides a numerical value for AML risk, ranging from 0.60 to 0.79, and categorizes it into levels like Very High, High, Medium, and Medium/High based on the numerical value.

The table visually represents AML risk levels in the banking sector, with a medium risk value of 0.60 and a higher risk value of 0.75 for casinos, indicating their risk levels. This information is useful for financial analysis and regulatory compliance, assisting organizations in effectively managing their AML risks.

Challenges Faced by the Financial Sector

The financial sector in Suriname faces challenges in adopting a uniform, risk-based approach across institutions and DNFBPs. This leads to vulnerabilities and a lack of comprehensive compliance with AML/CFT regulations, diminishing protection against financial crimes.

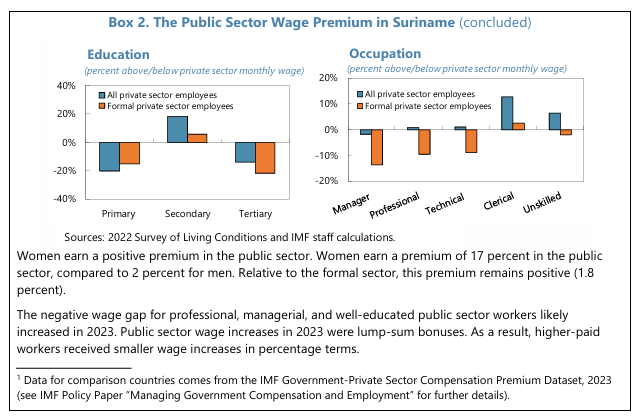

Image source: Public sector wage premium in Suriname

The wage premium in Suriname’s public sector, particularly for those with tertiary education or managerial roles, can impact AML/CFT efforts and financial institutions’ consideration of corruption and money laundering. Understanding wage dynamics helps assess risks and implement controls, enhancing the financial system’s integrity. Addressing this wage premium is crucial for job security and benefits, ensuring a competitive private sector.

An Assessment Team classified FIs and DNFPBs in Suriname based on their importance, materiality, and ML/TF vulnerability. The report’s conclusions assigned a stronger weighting to AML/CFT systems in more important sectors than those of less importance.

Regulatory Obligations for Both FIs and DNFBPs

Suriname’s financial institutions should implement a robust Anti-Money Laundering/Countering the Financing of Terrorism (AML/CFT) program, incorporating customer due diligence, transaction monitoring, and reporting procedures. Risk assessments are required to identify and understand risks associated with money laundering and terrorist financing, and institutions must pay attention to suspicious transactions and report unusual activities to authorities.

DNFBPs must adhere to AML/CFT regulations, including customer due diligence measures, especially for politically exposed persons (PEPs). They also maintain client and transaction records to ensure reporting requirements and prevent money laundering activities, mirroring the obligations of financial institutions.

FIs and DNFBPs must maintain internal controls and training programs to comply with AML/CFT regulations, establish procedures for identifying and reporting suspicious transactions, and ensure adequate disclosure measures when forming business relationships.

The Central Bank of Suriname (CBvS) regulates and supervises FIs and DNFBPs, ensuring compliance with AML/CFT obligations. Regular audits and inspections are conducted, and institutions failing to meet these obligations may face sanctions and penalties.

Financial institutions and non-financial businesses in Suriname must implement and enforce regulatory measures such as thorough due diligence, effective record-keeping, personnel training, and prompt reporting of suspicious activities to protect the financial system from misuse by criminal entities and meet international AML/CFT standards.

Challenges and Progress in Suriname’s Fight Against Money Laundering and Terrorism Financing

Suriname‘s financial institutions are actively combating money laundering and terrorism financing, but systemic weaknesses and regulatory deficiencies persist despite significant progress in addressing these issues.

Suriname is enhancing its AML/CFT framework by establishing the Act on Preventing and Combating Money Laundering and Terrorist Financing, and the Central Bank of Suriname is enhancing its supervisory powers and regulatory guidance for financial institutions.

Suriname’s commercial banks are improving customer due diligence and international standards but face criticism for prioritising profit over compliance. The Financial Intelligence Unit (FIU) is collaborating with non-financial businesses to improve AML/CFT compliance, but its effectiveness is hindered by public corruption and lax enforcement.

The Caribbean Financial Action Task Force (CFATF) has identified significant deficiencies in Suriname’s AML/CFT regime. These deficiencies highlight the country’s struggle with effective implementation and monitoring due to political will and institutional capacity. The CFATF is under international pressure to address these strategic deficiencies to avoid potential countermeasures affecting financial institutions and international relationships.

Image source: Financial crime

Adoption of Risk-Based Customer Due Diligence (CDD) and Record-Keeping Measures

A report reveals that while some financial institutions have implemented risk-based customer due diligence (CDD) and record-keeping practices, the level of implementation varies. Larger institutions have robust CDD frameworks, while smaller institutions and certain DNFBPs, like real estate agents and precious metal dealers, are less consistent in applying these measures. This uneven adoption of CDD practices leaves gaps in the country’s defenses against money laundering and terrorist financing.

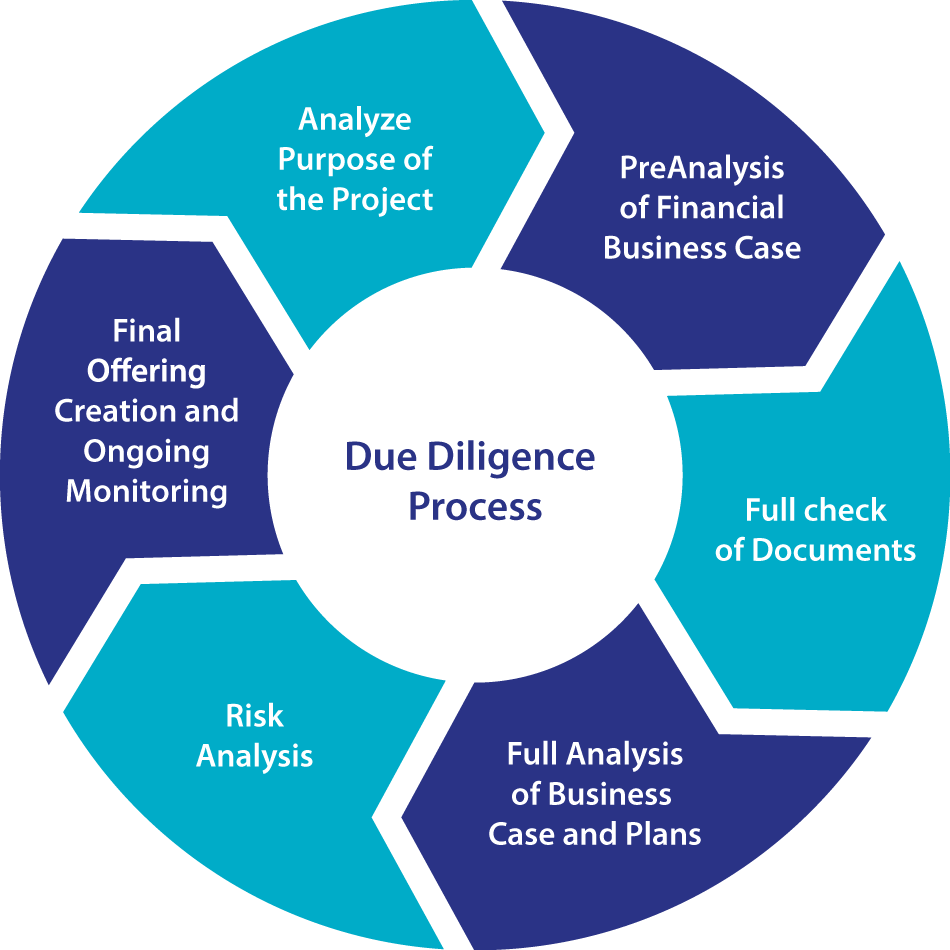

Image source: Due diligence process

Varying Levels of Compliance and Understanding of Obligations Across Financial Institutions and Businesses

One evaluation reveals varying levels of compliance with AML/CFT requirements across financial institutions and DNFBPs. Larger banks often demonstrate better compliance due to resources and technical expertise, while smaller businesses, particularly DNFBPs, lack awareness and resources. Many businesses don’t understand the importance of beneficial ownership identification or enhanced due diligence for high-risk clients. Limited training on AML/CFT compliance further contributes to the knowledge gap in these sectors.

Actions Taken by the Government

The Surinamese government under Samntokhi is enhancing its anti-money laundering and counter-terrorist financing framework to improve compliance with international standards and address deficiencies, fostering a secure financial environment.

The WMTF Act, enacted in November 2022, aims to enhance Suriname’s regulatory framework for AML/CFT measures by providing clear guidelines and requirements for financial institutions to follow in their operations.

Suriname is enhancing customer due diligence in its financial sector by mandating financial institutions to conduct more thorough KYC checks to manage risks related to money laundering and terrorist financing.

The government has emphasised the significance of the financial intelligence unit (FIU) in implementing AML/CFT measures. Since June 2024, it has received membership in the Egmont Group to enhance international collaboration and access necessary training and resources.

The Surinamese government is partnering with international organizations like CFATF to enhance its AML/CFT compliance, providing technical assistance, training, and workshops to enhance the capacity of regulatory bodies and financial institutions.

Suriname is enhancing its AML/CFT measures and actively reporting to the CFATF on progress in rectifying deficiencies identified in mutual evaluation reports. This has led to a re-rating of several FATF Recommendations as part of its commitment to continuous improvement.

Central Bank van Suriname

In Suriname, the Central Bank (CBvS) plays a crucial role in identifying violations of anti-money laundering (AML) and counter-terrorist financing (CFT) regulations during on-site inspections. Upon detection of deficiencies in financial institutions (FIs), the CBvS communicates these issues, requiring FIs to develop and submit an action plan for remediation.

Image source: Central Bank of Suriname

The Central Bank of Suriname detects AML/CFT violations during on-site inspections and promptly communicates these deficiencies to relevant financial institutions for corrective action. After being informed of deficiencies, financial institutions must create an action plan outlining the steps to rectify the issues, ensuring a structured approach to compliance and remediation within set timeframes.

The CBvS regularly meets with financial institutions’ supervisory boards and management to evaluate deficiencies and monitor the progress of action plans. This ensures accountability and facilitates necessary improvements to ensure continuous improvement.

Suppose a financial institution fails to comply with the CBvS recommendations. In that case, the bank may instruct them to follow a specific conduct line to ensure compliance with AML/CFT regulations and maintain the integrity of Suriname’s financial system.

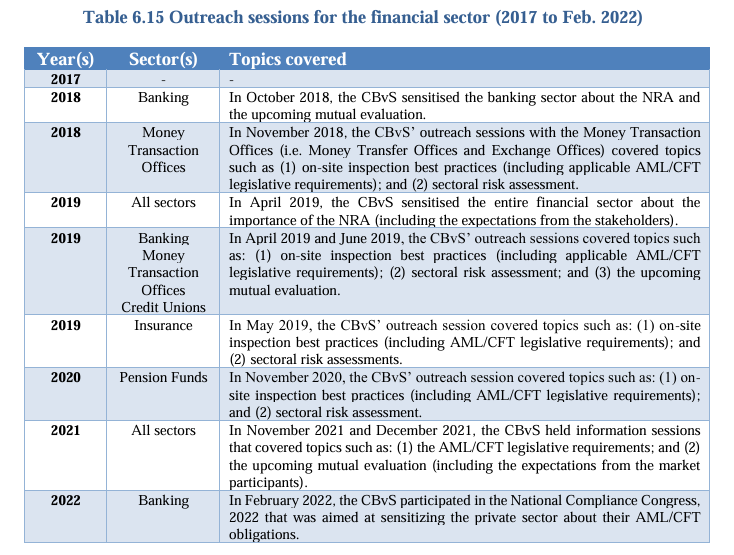

Image source: Outreach sessions

Roles of FIs and DNFBPs in the Context of Preventing Financial Crimes

Image source: Types of financial crimes

Financial institutions (FIs) such as banks and credit unions play a crucial role in preventing financial crimes by managing client funds, conducting due diligence, verifying identities, understanding financial activities, monitoring transactions for suspicious activity, ensuring compliance with AML/CFT regulations, and maintaining extensive record-keeping practices for investigations.

DNFBPs, such as real estate agents, casinos, and legal professionals, operate in sectors not typically considered financial institutions but face risks of exploitation for illicit activities. Their primary role is customer due diligence, reporting suspicious transactions, and implementing internal controls and training programs to ensure compliance with AML/CFT obligations.

FIs and the DNFBPs are key in enhancing Anti-Money Laundering and Combating Terrorism Financing (AML/CFT) strategies. FIs monitor large-scale transactions and enforce regulatory frameworks, while DNFBPs act as gatekeepers in sectors prone to illicit financing, reducing economic risks.

Potential Risks of FIs and DNFBPs Failure to Comply

Non-compliance with AML/CFT regulations can lead to severe legal penalties for FIs and DNFBPs, including fines and sanctions. Suriname’s regulatory bodies can impose sanctions against institutions that fail to comply, potentially resulting in legal proceedings and potential criminal charges.

Non-compliance with regulations can lead to fines, increased scrutiny, and future costs, affecting financial implications like revenue loss or difficulty maintaining international partnerships. It can damage institutions’ reputations and deter customers, investors, and partners, leading to business loss and market share. Compliance failures can cause operational challenges and regulatory-mandated remedial measures.

Impacts of poor AML compliance

Suriname’s financial system’s integrity is at risk due to widespread non-compliance among FIs and DNFBPs. This could increase the risk of money laundering and terrorism financing, international sanctions, and economic instability. Additionally, being designated a high-risk jurisdiction could result in wider economic repercussions.

The failure of FIs and DNFBPs in Suriname to comply with AML/CFT regulations poses significant legal, financial, operational, and reputational risks, impacting the institutions directly involved and the broader financial system and economic stability.

Sectoral Responses

Suriname is implementing measures to improve compliance with Anti-Money Laundering and Combating the Financing of Terrorism standards to combat money laundering and terrorist financing, particularly amid increasing oil discoveries and economic challenges.

Extractive Industry

Suriname’s economy heavily relies on the extractive sector, with oil and gold accounting for 85% of exports and 27% of national revenues. However, corruption and lack of transparency in concession awards pose challenges. The government is implementing clearer processes and stronger oversight.

Image source: Suriname’s oil exploration challenges (Bloomberg)

Legislative Framework Updates

Suriname has implemented new laws and amended existing ones to comply with international standards on AML/CFT. Significant improvements include criminalizing money laundering and terrorist financing and creating a legal framework for policy implementation. However, further legislative reforms are needed to address the remaining deficiencies identified by the Caribbean Financial Action Task Force.

Capacity Building and Training Programs

Targeted capacity building and training programs are being initiated to enhance understanding of AML/CFT risks and compliance obligations across the public and private sectors, aiming to empower stakeholders in combating financial crimes related to the burgeoning oil industry.

Public-Private Partnerships

Government and private sector collaboration is being promoted to combat money laundering and terrorist financing. Public-private partnerships are being emphasised for enhanced information sharing, improved compliance mechanisms, and joint actions to mitigate financial system risks.

Suriname is enhancing its Anti-Money Laundering (AML) and Combating the Financing of Terrorism (CFT) frameworks to protect its financial system, especially as oil sector revenues increase. By improving regulatory oversight and collaborating with international bodies, the country aims to address financial crime vulnerabilities, boost investor confidence, and ensure global compliance, ensuring long-term economic and financial stability.

Recommendations for Improving Sectoral Compliance and Risk Mitigation

To strengthen sectoral compliance and mitigate risks, we suggest several key recommendations:

Enhancing Awareness and Training: Training programs should educate financial institutions and DNFBPs on AML/CFT obligations, emphasising risk indicators, effective CDD measures, and record-keeping importance.

Image source: Strategic themes to strengthen AML/CFT framework

Promoting a Risk-Based Approach: Authorities should encourage a risk-based approach across all sectors, requiring financial institutions and DNFBPs to create risk assessment frameworks that consider client nature, business models, and geographic exposure to ML/TF risks.

Improving Supervisory Oversight: Regulatory bodies should conduct regular audits and inspections to ensure compliance with AML/CFT measures, especially for smaller entities lacking fully integrated measures.

Encouraging Technological Integration: Automated transaction monitoring systems can improve compliance by enabling institutions to detect suspicious activities more effectively.

Suriname’s financial institutions and designated non-financial businesses and professions (DNFBPs) play a vital role in the country’s efforts to combat money laundering and the financing of terrorism (AML/CFT). However, notable challenges need to be addressed to improve the effectiveness of these efforts.

Strengthening Suriname’s Defenses Against Financial Crime

To strengthen Suriname‘s defenses against financial crimes, several key areas require attention:

Awareness: All stakeholders involved must increase their awareness of AML/CFT regulations and the risks associated with financial crimes.

Training: Providing comprehensive training programs for financial institutions and DNFBPs can ensure that personnel are well-equipped to identify and respond to suspicious activities.

Supervision: Enhanced supervisory mechanisms are crucial to ensuring compliance with AML/CFT regulations and holding institutions accountable.

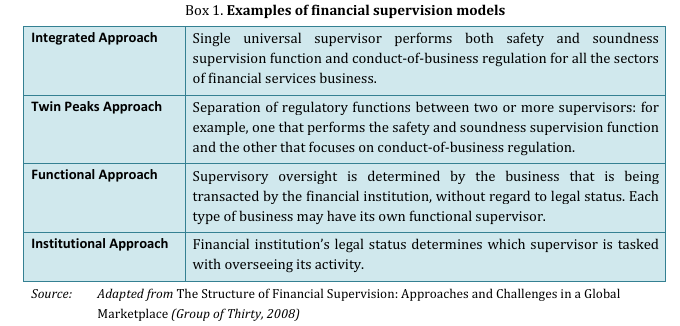

Financial supervision models – Examples

Risk-based approach: Promoting a consistent approach allows institutions to allocate resources effectively based on the specific risks they face.

By addressing these gaps, Suriname can significantly improve its AML/CFT framework, thereby enhancing the overall integrity and safety of its financial system. This proactive stance mitigates risks and strengthens the nation’s capability to combat financial misuse effectively.

Curbing Casino Issues in Suriname

The casino sector in Suriname should improve its regulatory frameworks, enhance compliance, foster stakeholder collaboration, and strengthen monitoring measures to combat AML/CFT and financial crime risks.

The FATF Recommendation 27 suggests a robust regulatory framework for casinos, including clear responsibilities, compliance requirements, detailed guidelines on customer due diligence, suspicious transaction reporting, risk assessment procedures, and regular employee training.

Casinos should cooperate closely with the Financial Intelligence Unit (FIU) in Suriname to combat money laundering and terrorist financing effectively. Regular communication between the two organisations will help identify and address potential risks, enhancing the sharing of relevant information.

Regular audits and inspections are crucial for casinos to assess compliance with AML/CFT regulations, identify vulnerabilities, and establish accountability. Public awareness of these measures can improve transparency, promote responsibility, and enhance the casino environment.

Investing in advanced technology solutions like transaction monitoring systems can help casinos detect suspicious patterns in real time, automate compliance processes, enhance record-keeping, and ensure timely reporting to authorities.

Curbing Terrorist Financing Issues in Suriname

Suriname is addressing terrorist financing challenges by strengthening its regulatory framework, but continuous monitoring and enhancement of compliance mechanisms are necessary to mitigate risks effectively.

Suriname is improving its Anti-Money Laundering and Combating Financing of Terrorism (AML/CFT) regime to comply with international standards, implement legislative amendments, and establish a framework to address terrorist financing. However, strategic deficiencies in the AML/CFT framework could exploit gaps for terrorist financing, prompting the Caribbean Financial Action Task Force’s concern.

Internal AML compliance controls

Suriname’s financial institutions are advised to adopt a risk-based strategy to detect and mitigate terrorist financing risks. This strategy requires effective customer due diligence and timely reporting of suspicious transactions. The government and Financial Intelligence Unit are enhancing compliance with non-financial businesses, but vulnerabilities in financial and regulatory systems may still allow misuse.

Suriname must strengthen its international cooperation and participation in global efforts to combat terrorist financing by sharing intelligence and best practices related to AML/CFT, thereby enhancing its capabilities.

Conclusion

Suriname is improving its AML/CFT framework through legislation, regulatory enhancement, and international collaborations, but systemic weaknesses persist. Failure to adhere to anti-money laundering and counter-terrorist financing regulations can pose significant risks to financial institutions and the country.

Suriname’s casinos are implementing strict regulations to combat money laundering and terrorist financing. They are enhancing cooperation with regulatory bodies, conducting regular audits, raising public awareness, and utilising technological advancements to combat terrorist financing.

Suriname’s financial institutions are crucial in preventing fraud and identifying suspicious activities. Collaboration between government, regulatory bodies, and institutions aligns with international AML/CFT standards. Continued vigilance and adaptation are needed to maintain Suriname’s positive trajectory in combating money laundering and terrorist financing.

Under the leadership of President Chandrikapersad Santokhi, the Surinamese government has made remarkable strides in strengthening anti-money laundering measures, showcasing a commitment to financial integrity and transparency. These progressive steps enhance Suriname’s global standing and lay a solid foundation for a more secure and prosperous economic future.

Explore Our Archive of Surname-related Articles:

- Dilip Sardjoe: The Business Socialist Who Shaped Suriname’s Economy and Politics

- Celebrating Powerful Women of Suriname: Figures Who Are Making a Difference

- Strengthening Financial Integrity: The Santokhi Administration’s AML/CFT Initiatives in Suriname

- Overview of Suriname’s AML/CFT Measures and Key Findings

- How Globalization is Shaping Business Culture in Suriname

- AML/CFT in Suriname: Challenges Faced by Financial Intelligence and Investigative Systems under President Santokhi

- AML/CFT Framework in Suriname: Legal and Regulatory Gaps

[…] institutions to ensure compliance with AML/CFT regulations. They will establish an independent financial intelligence unit, enforce stricter penalties for non-compliance, require financial institutions to maintain detailed […]