In the quiet boardrooms and sun-drenched family offices of the world, the conversation around wealth is shifting. It is no longer a simple discussion of how much wealth or what returns it generates. Instead, a deeper, more human set of questions has taken center stage: How do we keep a family safe across borders? How do we hold a business together when it spans three continents? How do we protect a lifetime of work from the friction of modern regulation?

Wealth, it turns out, is not only about money. It is about the stories and legacies of the people who built it. Mauritius is increasingly discussed not just as a financial center, but as a place where families and their advisers can think more clearly about how wealth moves across borders. Within that context, the emergence of SILIB, Structured Investment-Linked Insurance Business, is less a technical product launch than an answer to a broader human question: how do families protect what they have built while staying flexible in an uncertain world?

The scale of that question is hard to overstate. Forbes counts 3,428 billionaires worldwide controlling a combined $20.1 trillion, including 390 new entrants in the last year alone. Nowhere is that wealth moving faster than the Gulf: Knight Frank projects the UAE’s population of ultra-high-net-worth individuals to grow 36% by 2031, to nearly 5,000 people. Wealth, in other words, is not just growing, it is concentrating and migrating at the same time, and the infrastructure built to manage it has had to migrate with it.

Table of Contents

The New Global Complexity

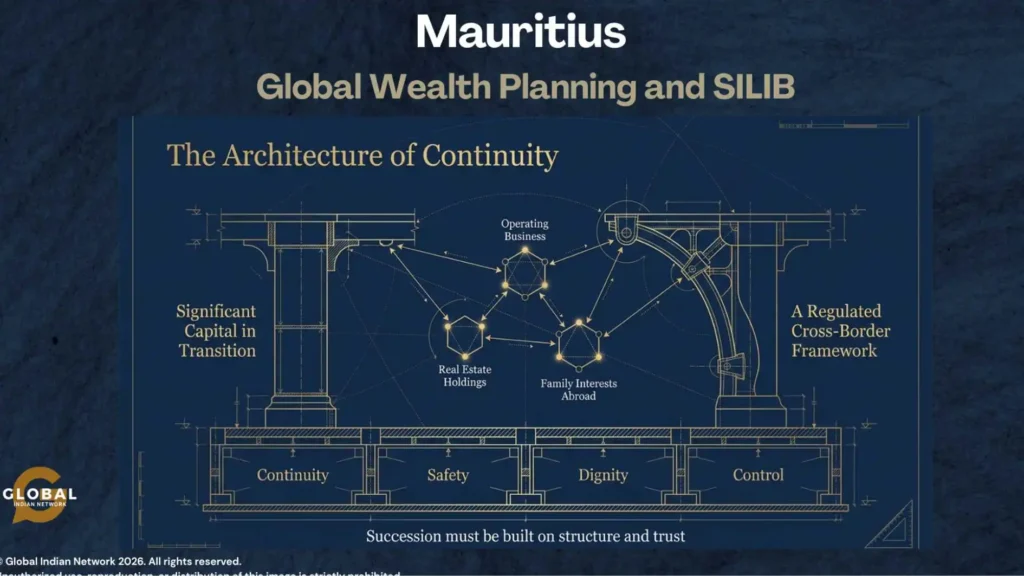

The world has changed for the modern migrant entrepreneur and the globally mobile professional. A family based in Dubai may have manufacturing interests in India, a vacation home in Mauritius, and children studying in London or Singapore. Traditional, single-country planning models often buckle under that level of complexity, they were built for a world where wealth, and the people who held it, stayed in one place.

That single sentence, interests here, a home there, children somewhere else entirely, describes a growing share of the world’s wealthy families, not a small minority of unusually complicated ones. Mobility used to be the exception that estate planners footnoted; today it is closer to the default. A family’s residency, its business operations, and its heirs’ lives increasingly sit in three or four different legal systems at once, each with its own tax rules, succession law, and reporting requirements. Trying to manage that with a single domestic will or a structure designed for a single jurisdiction is a bit like trying to run an international business out of a single filing cabinet.

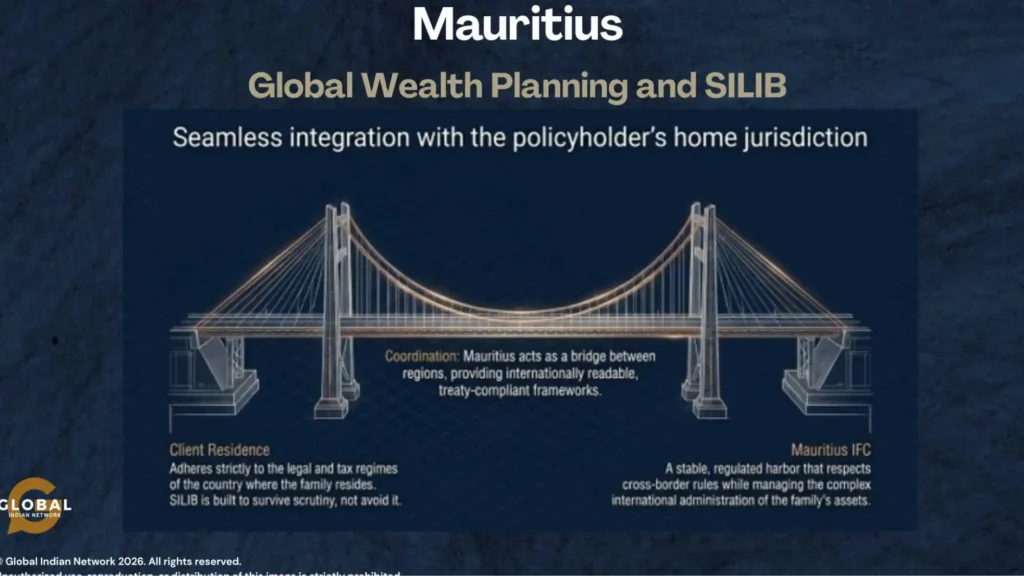

This is where Mauritius is carving out its role: as a bridge between the Global South and the rest of the world. The island is positioning itself as a practical way to manage cross-border wealth through a regulated, transparent structure, one built to survive legal scrutiny while still serving a family’s long-term goals.

Understanding SILIB: Trust Over Mystery

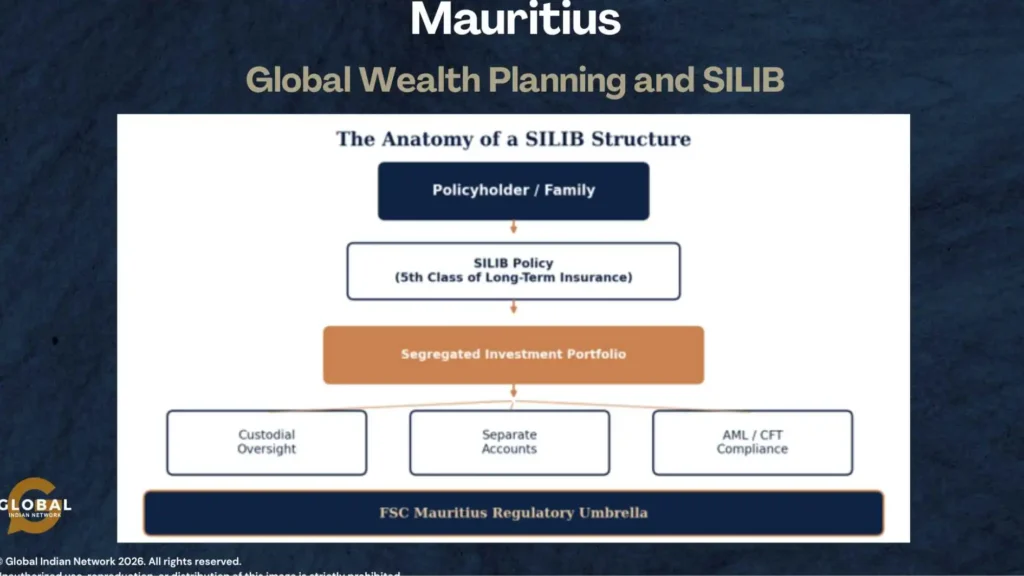

For many people, financial structures feel like black boxes: complex, opaque, and built on mystery. SILIB, introduced in 2022 as the “fifth class” of long-term insurance under Mauritian law, is designed to replace mystery with clarity.

Technically, a SILIB policy is backed by a segregated investment portfolio with custodial oversight, separate accounts, and strict AML/CFT compliance. But the human meaning is simpler: people want wealth structures they can trust. In an era when transparency has become the new gold standard, having a structure governed by the Financial Services Commission (FSC) of Mauritius offers a level of legal clarity that matters as much to families as the returns themselves.

Speed Matters: Contractual Continuity vs. Probate

One advantage of this structure is easy to miss on a first read, but it tends to be the one that matters most when a family actually needs it: speed at the moment of transition. A traditional inheritance, run through a will and an operating company’s shareholding, typically has to pass through probate, a court process that can take months or years, freeze assets at the worst possible time, and vary unpredictably between jurisdictions.

A SILIB policy, by contrast, is a contract. Beneficiary designations sit inside the policy itself, so a triggering event can release assets to the next generation in a matter of days, not years, without the underlying portfolio ever being commingled with an estate in probate. For a family already managing grief, that difference is not a technicality; it is the difference between a transition and a crisis.

By the Numbers: A Growing Ecosystem of Stability

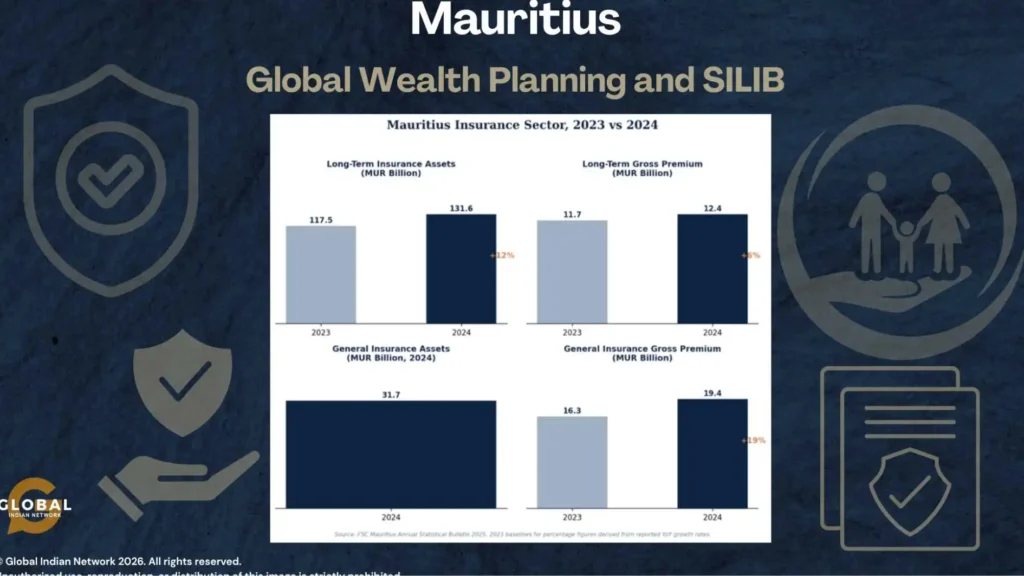

The shift toward Mauritius is not just a feeling; it is backed by measurable growth across the island’s financial sector. According to the FSC Mauritius Annual Statistical Bulletin 2025, the insurance and global business sectors are reaching new heights:

• Total assets in long-term insurance reached MUR 131.6 billion in 2024, a 12% increase on the prior year, while gross premiums rose to MUR 12.4 billion, up 6%.

• The general insurance sector held MUR 31.7 billion in assets, with gross premiums climbing 19% to MUR 19.4 billion, the fastest-growing segment of the market.

• Corporate and trust service providers, the firms that actually administer structures like SILIB, now manage USD 489 million in total assets (up 10% year-on-year) and generated USD 381 million in income (up 8%).

• There are 13,289 live Global Business Company (GBC) licenses and a further 6,385 Authorised Companies, giving the jurisdiction one of the largest pools of international corporate substance of its size.

• Mauritius climbed to 50th place globally in the Global Financial Centres Index (GFCI 39), gaining eight positions in a year and reinforcing its growing standing as an international financial centre.

Taken together, these figures describe an ecosystem with genuine depth on both sides of the ledger, not just assets under management, but the licensed companies, trust administrators, and professionals needed to actually run them. With over 13,000 live GBC licenses and thousands more Authorised Companies, Mauritius is no longer a hidden gem; it has become a primary hub for international substance.

Case Study: The Multi-Generational Bridge

The Indian Manufacturing Family

Picture a family that built a successful manufacturing business in India. The parents now keep a second home in Mauritius, while their adult children work in the UK and Singapore. Their wealth is a tangled web of ownership, succession, and tax exposure spread across four jurisdictions. Using a tool like SILIB, the family can create a coordination mechanism: assets stay ring-fenced and professionally managed under a single regulated framework, so the handover of wealth to the next generation does not become a legal or emotional crisis.

What makes this scenario familiar to so many advisers is not the manufacturing business itself, but the shape of the problem. The parents understand the business; the children, scattered across different careers and time zones, may not. Without a coordinating structure, succession conversations tend to happen too late, under pressure, and informally, which is exactly when family disagreements are most likely to harden into disputes. A regulated framework gives the conversation somewhere to happen earlier, on calmer terms.

The GCC Generational Transfer

In the Gulf, Strategy& estimates that families may transfer between $500 and $700 billion to the next generation by 2035, with roughly $200 to $250 billion of that potentially moving offshore. For a family in Riyadh or Dubai, the challenge is the same one facing the Indian manufacturing family: succession needs structure, and structure needs trust. Whether they choose to diversify internationally or keep assets close to home, these families need a framework their heirs can actually read and that regulators will respect.

Choosing Mauritius: What Families Tend to Weigh

Advisers who work with globally mobile families report a fairly consistent checklist when a structure like SILIB enters the conversation:

• Does the jurisdiction’s regulator have a credible track record, rather than a marketing claim, of enforcing transparency and AML/CFT rules?

• Will the structure be recognized and respected by tax authorities in every country where the family has assets, residency, or heirs?

• Can the structure hold a genuine mix of assets, an operating business, real estate, listed investments, without forcing the family to unwind what they have already built?

• Is there a clear, professionally managed custodial chain so that no single individual’s judgment is the only thing standing behind the family’s wealth?

• Does the cost and complexity of the structure match the complexity of the family’s actual life, rather than adding a new layer of opacity on top of an old one?

SILIB is not the only way to answer these questions, and it will not suit every family. But the fact that the questions themselves have become this consistent, across families in India, Africa, and the GCC, says something about how mainstream cross-border planning has become.

The Role of the Modern Adviser: From Sales to Education

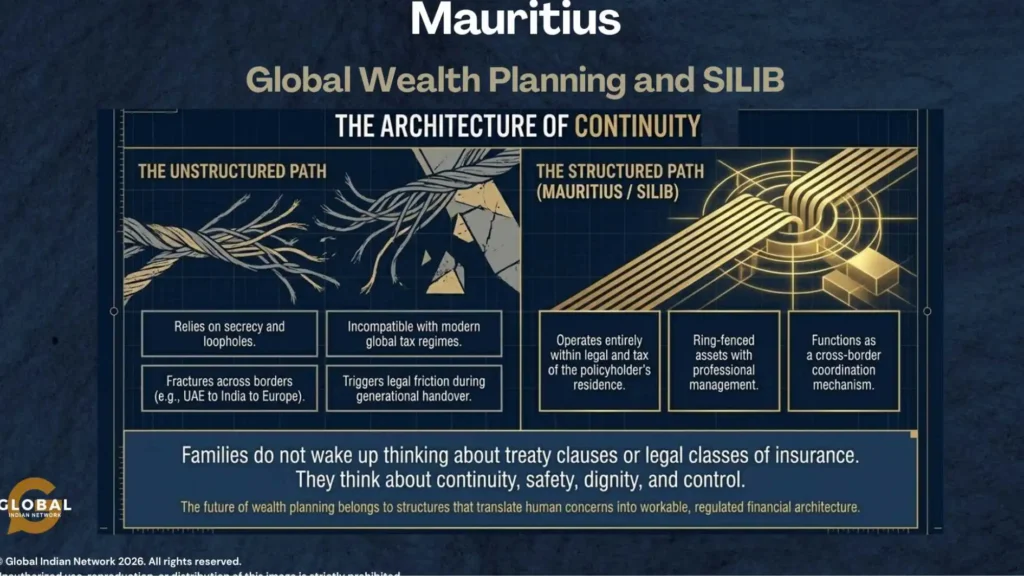

In this environment, the role of the wealth adviser has evolved. Families do not wake up thinking about treaty clauses or legal classes of insurance. They think about continuity, safety, dignity, and control.

The most effective advisers are the ones who can translate those human concerns into workable financial architecture. That is why education has become so central to this market: platforms dedicated to SILIB are now offering technical guides, Double Taxation Agreement (DTA) analyses, and CPD-accredited modules. A market that needs to be taught before it can be sold to is usually a market whose real opportunity is still in its early, most valuable stages.

Compliance as Comfort, Not a Burden

There was a time when “offshore” was treated as a synonym for “hiding.” Those days are largely over. Modern wealth planning is about building frameworks that can survive the most intense legal scrutiny, not evade it.

SILIB is intended to be used in full accordance with the tax regime of the policyholder’s country of residence. It is not about chasing loopholes; it is about peace of mind. Knowing a structure is compliant and transparent frees a family to focus on what actually matters to them: their business, their philanthropy, and their future.

A Global Benchmark: Where Mauritius Stands

Mauritius’s regulators are explicit that the island’s standing should be judged against established peers, Singapore, Luxembourg, and Bermuda, rather than viewed in isolation. The comparison matters because it reframes the conversation: this is not a local financial story, but an internationally readable framework competing on the same terms as the world’s most established hubs.

The FSC’s strategic plan for 2024–2027 is built on three pillars, innovation, compliance, and sustainable finance, aimed squarely at strengthening that international standing while keeping the products it champions, such as SILIB, grounded in rules, reporting, and legal clarity rather than mystery.

Conclusion: The Future of Thoughtful Wealth

The deeper story behind SILIB and the growth of the Mauritius IFC is not about a single jurisdiction or a single legal instrument. It is a story about how wealth itself is maturing.

As families become more global, the tools they rely on must become more thoughtful, transparent, and adaptable. Mauritius has positioned itself at the heart of that shift, offering a regulated and practical way for people to live across borders without losing clarity or control.

None of this removes the hard work of planning a family’s future, the difficult conversations between generations, the negotiations between siblings, the slow process of building trust between heirs who may barely know one another. What a well-built structure does is give that work somewhere stable to happen, instead of forcing families to invent the rules as they go.

Ultimately, the future of wealth planning belongs to those who recognize that behind every portfolio, there is a human story still waiting to be protected.

————————————————————————————————————

Sources: FSC Mauritius Annual Statistical Bulletin 2025; FSC Mauritius Strategic Plan 2024–2027; Global Financial Centre Index 36 (GFCI 36); Forbes World’s Billionaires List; Knight Frank Wealth Report; Strategy& GCC wealth transfer estimates.